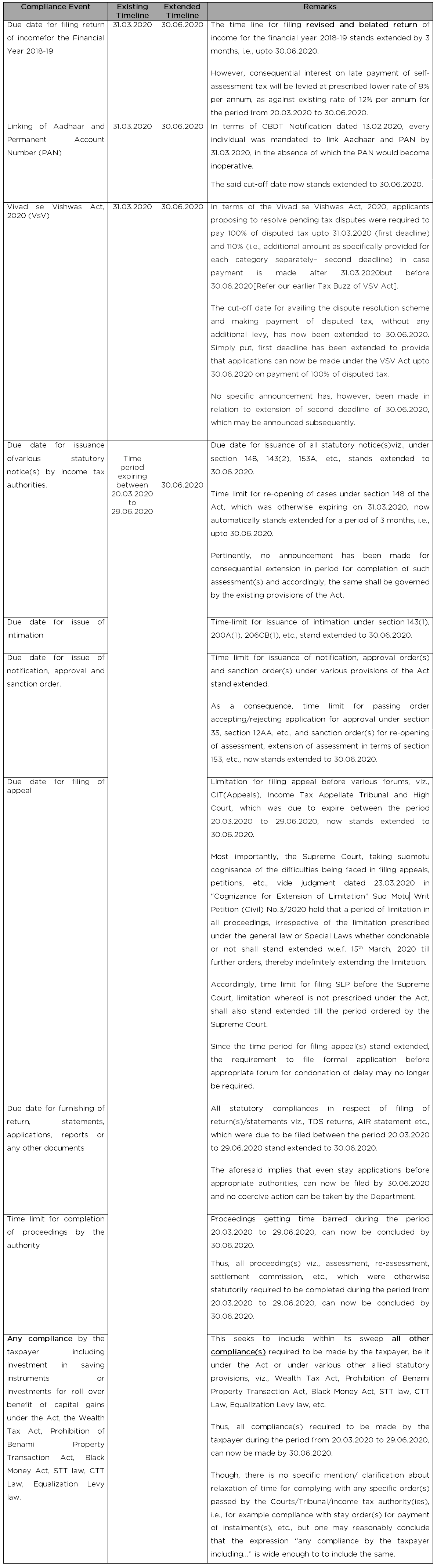

The Securities Appellate Tribunal by way of its order dated February 27, 2020 has set aside the orders passed by the Insurance Regulatory and Development Authority of India (“IRDAI”) (passed on December 4, 2019 and December 27, 2019) wherein, it was held that invocation of pledge in respect of the shares of Reliance General Insurance Company Limited was null and void ab initio.

Facts

Appellant no.1, Nippon India Mutual Fund (“NIMF”) is a trust established under the Indian Trust Act, 1882. Whereas appellant no. 2, Nippon Life India Asset Management Limited (“Nippon AMC”) is an asset management company registered with the Securities and Exchange Board of India (“SEBI”). The respondent no.1 is the IRDAI. Respondent no.2, that is, IDBI Trusteeship Services Limited (“IDBI Trusteeship”) was appointed as debenture trustee in respect of non-convertible debentures (“NCDs”) issued by Reliance Home Finance Limited (“RHFL”). The appointment of IDBI Trusteeship as debenture trustee was made by way of a debenture trust deed dated January 10, 2018, entered into between IDBI Trusteeship and RHFL.

An information memorandum dated March 28, 2018 had been issued by RHFL for private placement of its 8000 NCDs aggregating to an amount of INR 400 crores. Nippon AMC subscribed to all 8000 NCDs at the time and is presently holding 6369 NCDs. However, RHFL was unable to redeem the NCDs on June 28, 2019 which was the maturity date, upon which, RHFL requested NIMF (one of the NCD holders) to restructure the terms of the NCDs and enable extension of the date of maturity from June 28, 2019 to October 31, 2019 (“Revised Maturity Date”).

The revision of the maturity date was agreed upon RHFL offering following additional securities: irrevocable and unconditional corporate guarantee offered by respondent no. 3, that is, Reliance Capital Limited (“Reliance Capital”), a promoter of RHFL; granting of put option right to the NCD holders, which required Reliance Capital to purchase NCDs in the event that the NCD holders were to exercise the put option; pledge by Reliance Capital in favour of IDBI Trusteeship over its entire shareholding in respondent no. 4, that is, Reliance General Insurance Company Limited (“RGICL”). RGICL, a subsidiary of Reliance Capital is in the business of general insurance. Pursuant to the aforesaid, a Guarantee Deed dated July 19, 2019 (“Guarantee Deed”) and a Share Pledge Arrangement dated June 26, 2019 (“SPA”) was executed by Reliance Capital whereby it pledged 100% of its shareholding which is RGICL shares (“RGICL Equity Shares”) in favour of IDBI Trusteeship. NIMF exercised its put option before the Revised Maturity Date, in order to sell 6369 NCDs. In that respect, NIMF issued a notice dated October 11, 2019, to Reliance Capital requiring purchase by the latter of the NCDs as per terms of the Guarantee Deed. However, when Reliance Capital failed to purchase the NCDs, NIMF wrote to IDBI Trusteeship seeking invocation of the pledged RGICL Equity Shares as per the terms of the SPA.

In pursuance thereto, IDBI Trusteeship issued notices dated October 18, 2019 and October, 24, 2019, to Reliance Capital, thereby invoking the pledge in respect of the RGICL Equity Shares. Thereafter, both IRDAI and the stock exchange were informed of the invocation of the said shares. However, the IRDAI by its order dated December 04, 2019 held that the aforementioned transfer of RGICL Equity Shares was null and void ab initio. Thereafter, an appeal had been filed before the Securities Appellate Tribunal, Mumbai (“SAT”) against the orders dated December 04, 2019 and December 27, 2019 (“Impugned Orders”).

By way of the Impugned Orders, IRDAI had held that the ‘transfer of shares’ made by IDBI Trusteeship, was in violation of Section 6A(4)(b)(iii) of the Insurance Act, 1938 (“Insurance Act”) which deals with approval of IRDAI in respect of registration of transfer of shares by public company carrying on life insurance business, general and health insurance business and re-insurance business, read with Regulation 3 (registration of transfer) of the IRDAI (Transfer of Equity Shares of Insurance Companies) Regulations, 2015 (“Transfer Regulations”). The IRDAI held that the aforementioned transfer of shares had been made by IDBI Trusteeship without the previous approval of the IRDAI and that such transfer, was void ab initio. By the order dated December 27, 2019, the IRDAI had reiterated its directions contained within the order dated December 04, 2019.

Further, by way of order dated December 27, 2019, the IRDAI additionally provided that such manner of transfer/pledge as aforesaid should not be given effect to, and that Nippon AMC and NIMF (collectively, “Appellants”) should exercise due diligence. An intervention application filed on behalf of Credit Suisse AG (one of the parties seeking enforcement of the SPA), was allowed in the interest of justice. The IRDAI had also held that the transfer had violated foreign direct investment regulations. Pertinently because both Credit Suisse AG and NIMF were foreign entities and foreign holding for an insurance company is capped at 49%.

Issue

Whether transfer/pledge of RGICL Equity Shares was in violation of Section 6A(4)(b)(iii) of the Insurance Act read with Regulation 3 of the Transfer Regulations.

Arguments

The Appellants contended that pursuant to the order dated December 04, 2019, by a representation dated December 12, 2019, they had informed the IRDAI that IDBI Trusteeship had only complied with its statutory duty by invoking the SPA and taking possession of RGICL Equity Shares.

IRDAI was also intimated by the Appellants that before finding a buyer and selling the RGICL Equity Shares, IDBI Trusteeship would make a formal application to the IRDAI. It was also contended that neither NIMF nor IDBI Trusteeship exercised any control over RGICL. Further, they also did not intend to exercise any control, make any changes or have a say in the management or the decision making process or exercise any voting rights in respect of RGICL. It was also contended that Nippon AMC was an asset management company which was carrying out its business activities as per Regulation 24 (restrictions on business activities of the asset management company) of the SEBI (Mutual Funds) Regulations, 1996.

IDBI Trusteeship pointed out that the RGICL Equity Shares were being held by it in a dematerialised account, only in its capacity as a debenture trustee and that the said shares had not been transferred to it. To that effect, an affidavit had also been filed by IDBI Trusteeship before SAT wherein, it provided an undertaking that prior to the transfer of the RGICL Equity Shares by way of sale, it would seek approval of the IRDAI.

Observations of the SAT

The SAT observed that the letter dated February 04, 2020 issued by the IRDAI (in response to being intimated by NIMF communication in respect of invocation of RGICL Equity Shares), had noted that the RGICL Equity Shares were being held by IDBI Trusteeship only in its capacity as a trustee. As such, the said shares had not been transferred to it. The aforesaid letter also advised the Appellants that as and when transfer of the said shares were being contemplated, Section 6A(4)(b)(iii) of the Insurance Act read with Regulation 3 of the Transfer Regulations would have to be complied with.

SAT noted that the aforesaid letter to the Appellants and the reply filed by IRDAI before the SAT were only damage control measures adopted subsequently to the Impugned Orders. Further, the stand taken by the IRDAI in their reply had only resulted in dilution of the Impugned Orders. Moreover, it was clear from the said reply that prior to transfer of the RGICL Equity Shares, the IRDAI was required to be in a position to carry out due diligence to ascertain: (i) fulfilment of the ‘fit and proper’ criteria; and (ii) the financial soundness of the transferee.

Decision of the SAT

The SAT noted that the contention of the IRDAI that the word ‘transfer’ under Section 6A(4)(b)(iii) of the Insurance Act would also include a transfer of shares including a pledge, would not be considered at the present stage. The SAT however, held that the direction in the Impugned Orders passed by the IRDAI, that the transfer/pledge of the RGICL Equity Shares was null and void ab initio was incorrect, and accordingly the Impugned Orders were set aside. It was also recorded by SAT that IDBI Trusteeship was holding the RGICL Equity Shares as a custodian and that it was to make endeavours to find a suitable buyer in respect of the said shares.

The SAT further held that when a suitable buyer would be found, an application would be made before the IRDAI to enable it to carry out due diligence and, inter alia, ascertain fulfilment of the fit and proper criteria. It was also clarified by the SAT that so long as the RGICL Equity Shares were held by IDBI Trusteeship in its capacity as a debenture trustee/custodian, it will not be able to exercise any control or make changes or have a say in the management or decision making process or exercise any voting rights in respect of the RGICL Equity Shares.

Vaish Associates Advocates View

The SAT did not consider if the word ‘transfer’ under section 6A(4)(b)(iii) of the Insurance Act would also include a transfer of shares including a pledge, and if one should seek approval from IRDAI at the time of, for example, pledging of RGICL Equity Shares.

However, it is pertinent to note that the SAT did in fact draw a conclusion that as and when a suitable buyer for the RGICL Equity Shares was in fact found, an application would have to be made before the IRDAI. This makes it amply clear that as and when the shares are to be transferred, ultimately, IRDAI Approval would have to be sought.

Further, it would be interesting to note that as per latest news reports, Vistra ITCL (formerly known as IL&FS Trust Company) has approached the Bombay High Court, in its capacity as the trustee of the secured redeemable nonconvertible debentures issued by Reliance Capital. Claiming a charge on the RGICL Equity Shares in lieu thereof, Vistra ITCL has sought to prevent NIMF, Nippon AMC and IDBI Trusteeship from dealing with the said shares. The decision of the Bombay High Court, could possibly queer the pitch for one of the parties’ in respect of finally dealing with the RGICL Equity Shares.

For more information please write to Mr. Bomi Daruwala at [email protected]